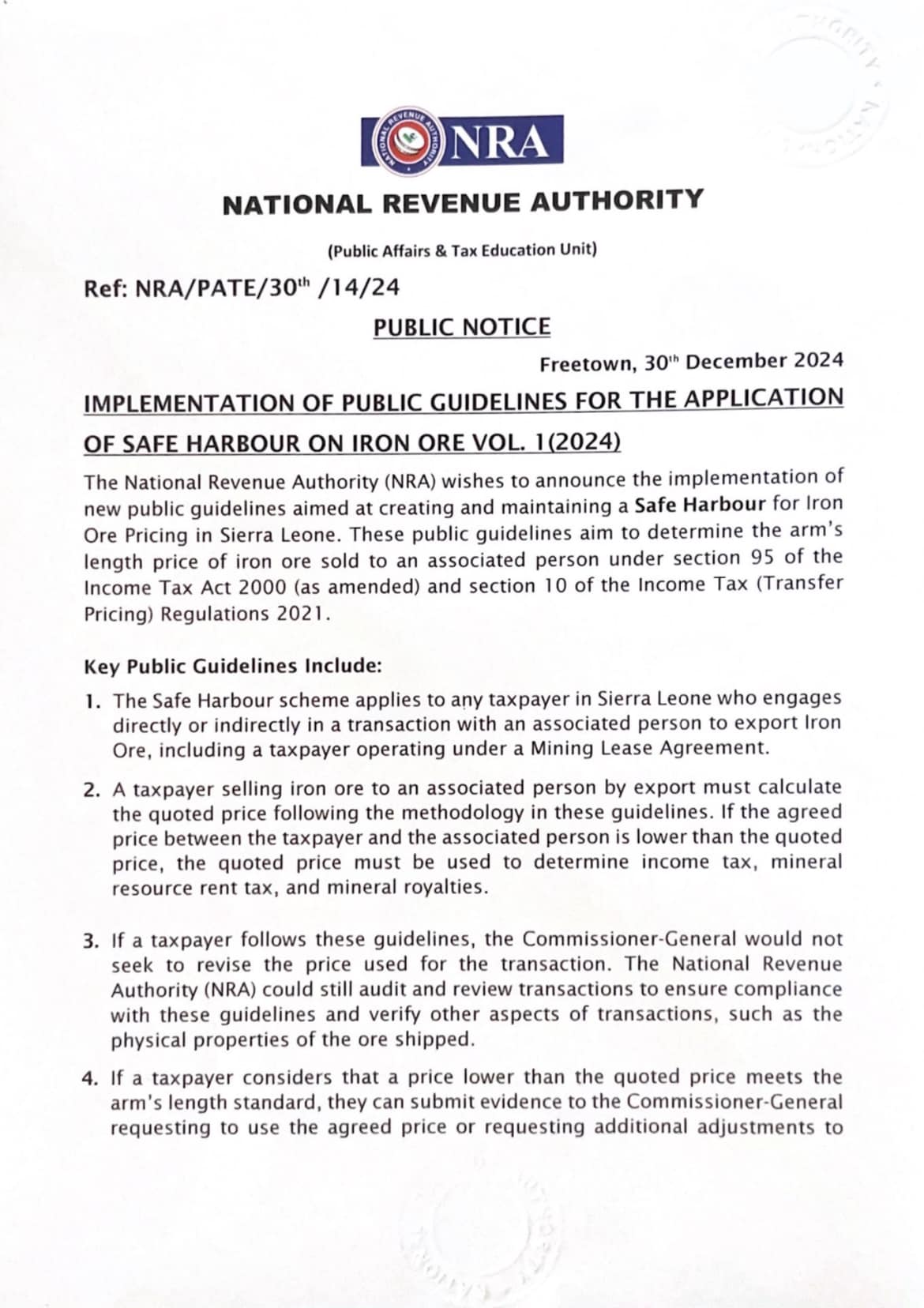

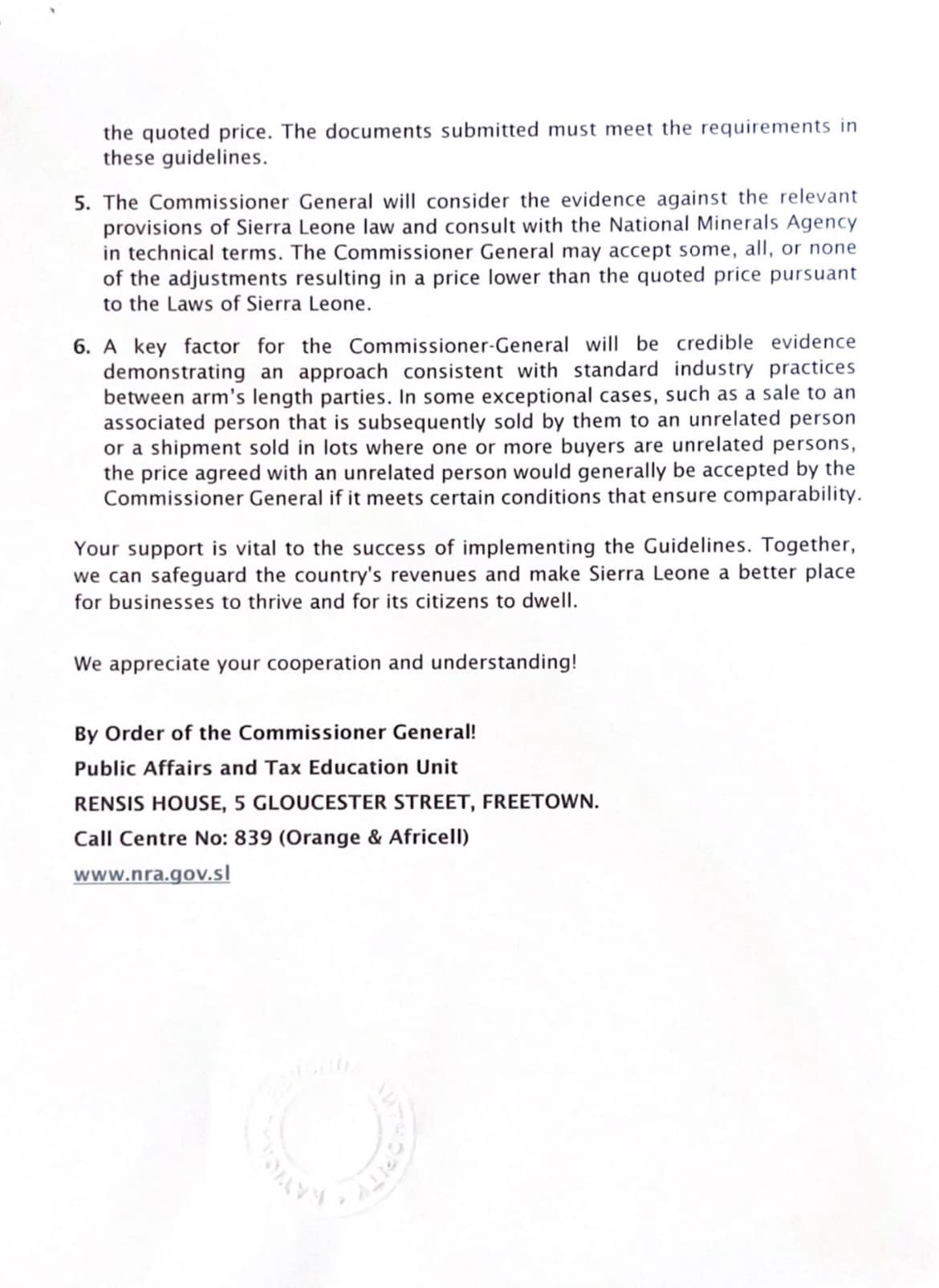

The National Revenue Authority (NRA) has unveiled new public guidelines to establish a Safe Harbour framework for determining the arm’s length price of iron ore transactions involving associated parties.

Effective from Volume 1 (2024), these guidelines aim to enhance compliance with section 95 of the Income Tax Act 2000 (as amended) and section 10 of the Income Tax (Transfer Pricing) Regulations 2021, fostering transparency and fairness in the iron ore sector.

See public notice: